.png?width=563&height=144&name=New%20GF%20Logo%20(37).png "New GF Logo (37)")

7 min read

March 22, 2024

.jpeg?width=824&height=549&name=AdobeStock_289579353%20(1).jpeg)

Most business leaders are familiar with their year-end financial closing process because it's closely associated with tax reporting.

|

Key Takeaways

|

Your year-end close, however, is not the only end-of-period financial process important to business operations.

In fact, each month, your business should execute a month-end financial close.

What Is a Month-End Close?

A month-end close is a set of bookkeeping and accounting tasks that are performed at the end of each month in a business to close out the month-long accounting period. Month-end close is an essential back-office process for the following reasons:

- Your business will be tax and audit-ready year-round.

- You'll have less mess and less stress at year-end.

- It's easier to identify and correct errors.

- You'll have accurate, reliable financial data for running your business throughout the year.

- You'll identify and correct areas that need improvement earlier.

Closing out your financial period each month can initially seem like an overwhelming job because of the number of tasks that must be handled. For this reason, it is strongly recommended that businesses create and use an accounting month-end close checklist. This will help you be certain your back office is current with your finances properly closed at the end of each month.

Your Month-End Close Checklist: 10 Best Practices for Month-End Close

1. Record All Income and Expenses

Ideally, you would be recording all transactions in real-time, as they occur so that this process will be complete by the time you begin your month-end close process. However, the first step in closing out your monthly financial period is to ensure that all of your income (sales, revenue, investment income, accounts receivable) and expense (invoices, bills, payroll, accounts payable) transactions have been recorded. You should also double-check that these records are accurate. Be sure to keep a file of all receipts for these transactions.

2. Complete Account Reconciliations

Once your transaction records are complete, you need to reconcile your records with the statements from all of your bank accounts and credit card accounts to make sure your balances, deposits, and withdrawals match your records. Look for discrepancies, errors, or signs of fraudulent transactions.

Additionally, you should also reconcile your payroll account to ensure all of your employee payments are correct. Take a close look at salary, wages, bonuses, commissions, and other benefits in addition to payroll taxes.

Read More: Financial Reports vs. Management Reports: What’s the Difference?

3. Balance Petty Cash

You must keep tabs on your petty cash fund (or funds, depending on how your business structures these accounts). For some businesses with lots of petty cash transactions, balancing the petty cash fund and filing receipts on a weekly basis might be the better strategy.

4. Review Fixed Assets and Liabilities

Create and update the list of all of your fixed and liquid assets, liabilities, amortization, and depreciation. Make note of any new asset purchases or sales. Also, be sure to document any new loans that the business has taken out and maintain a record and schedule of the company's loan payment progression on existing notes.

5. Take an Inventory Count

If your business is product-based, you should also take an inventory count at this time. In addition to checking the accuracy of your actual inventory against your records, you should also be reviewing which products are selling, how quickly they are selling, and whether or not you need to adjust your ordering and production schedule.

6. Prepare Your Financial Statements

Your business's basic financial statements are the primary deliverables generated during the month-end close. These financial reports include the income statement (profit and loss statement), balance sheet, and cash flow statement. These reports should be generated using a standardized process such as the generally accepted accounting principles (GAAP). Using a standardized process ensures your reports are easy to read and accurately comparable, month-over-month.

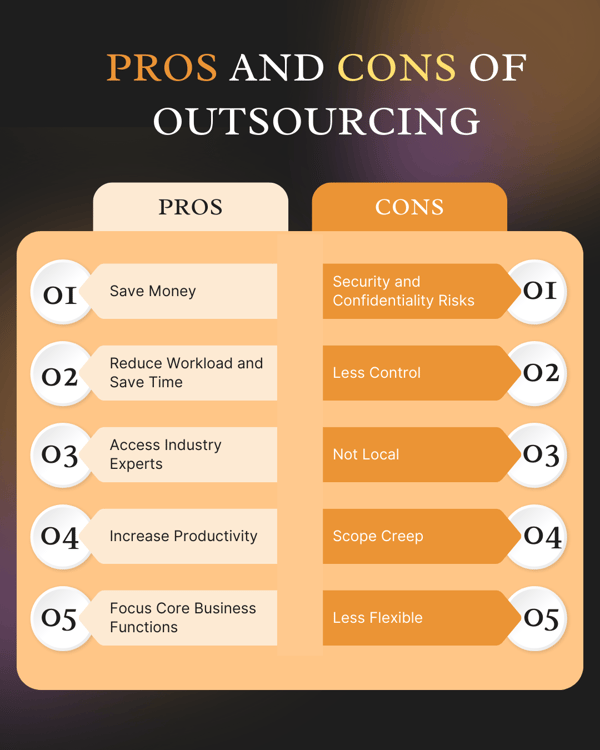

Read More: The Pros and Cons of Outsourced Accounting Services for Businesses

7. Prepare Your Management Reports

Management reports differ from financial reports because:

- They are not required by GAAP.

- They are generated on a discretionary basis.

- They are typically intended for internal purposes only.

Your management reports can include things like trailing twelve-month charts, key performance indicators, and other metrics that are useful in measuring and monitoring business performance and progress toward business goals.

Management statements should include the reports and metrics that are important to your unique business, its strategy, and its goals. Management reports should be monitored on at least a monthly basis to keep tabs on how well your business is performing and how effectively it is achieving its goals.

8. Review Your Numbers

Look over each of your reports and the data that was used to generate the numbers. You want to check for accuracy. (It might even be a good idea to ask another person to review the accuracy of your reports.) Additionally, you want to read the reports to understand your business's current financial health and performance over the past month.

In addition to looking at individual reports, revisit the reports from previous months to keep an eye out for trends in your numbers that could indicate upcoming cash flow problems, shrinking profit margins, an accumulation of unused capital, or other issues.

9. Revisit Your Budget

In addition to reviewing your financial reports, you should take time at the end of each month to revisit your budget and compare your budgeted (forecasted) numbers to your actual income and expense numbers. Are your actual numbers on par with the numbers you budgeted for? Are you spending more or less? Are you generating more or less revenue than projected?

If you notice any discrepancies between your budget and actuals, this represents a deviation from your financial strategy and plan. You must make changes and adjust your budget to get your business back on track and better aligned with the budget.

6 KPI Charts Every CEO Should Monitor

The One Page Scorecard Guide

[FREE DOWNLOAD]

10. Make Data-Driven Decisions

When reviewing all of your financial data during month-end close, you should constantly be asking questions about the business's performance and looking for signs of success and failure, leading indicators of potential challenges, progress toward goals, and upcoming challenges.

Keeping a close watch for these kinds of issues every month will help you make data-driven decisions to avoid and overcome challenges, take advantage of upcoming opportunities, and continuously improve your business's operations for improved efficiency, productivity, and profits.

Put Your Monthly Closing Checklist on Autopilot With Outsourced Accounting for Businesses

Month-end close comes with a long, work and time-intensive accounting checklist. For this reason, lots of businesses end up putting off the work associated with month-end close, and this leads to their back-office work falling behind and their financial data becoming increasingly inaccurate and unreliable.

In small and medium-sized businesses, especially, it can be difficult to keep up with the ongoing processes required to maintain a smoothly running back office and produce reliable financial and management reports. Plus, it's quite expensive to hire the in-house staff needed to create a well-run back office. In SMBs, the best solution to successful month-end close and a well-run back office is usually outsourced accounting for businesses.

With an outsourced team, your business will benefit from the automation of time-consuming back-office processes in addition to a whole host of advanced tools and technology designed to capture and organize your business's financial data. Plus, you'll have a complete team available to execute these time-consuming processes in addition to helping you understand and act on the results.